Updated October 2025

It’s a common misconception that anyone with assets isn’t eligible for Medicaid. In reality, 14% of all nursing home Medicaid applicants in 2012 had assets totaling over $100,000. New York requires those over 65 to report their income and assets (or “resources”) when applying for Medicaid. However, only some resources count toward the limit, and it only takes a little planning to ensure you’ll be eligible. Understanding which Medicaid assets are countable and which are exempt can help you protect your savings, qualify for benefits, and avoid unnecessary spend-downs.

At the Law Office of Andrew M. Lamkin, P.C., we know that the Medicaid application process can be daunting. Whether you’re planning for your future care or the care of an aging parent, we can explain the ins and outs of Medicaid eligibility. This page will help you begin to understand the importance of Medicaid countable and non-countable assets.

Understanding Medicaid Countable and Exempt Assets

Here are the key points to understand about Medicaid countable and exempt assets:

- ✓

Countable assets affect eligibility

Medicaid reviews income and resources to determine if you qualify. Assets that can be converted to cash—like savings, investments, and secondary property—count toward your limit.

- ✓

Exempt assets are protected

Your primary home, one vehicle, personal belongings, and certain funeral or burial funds are generally Medicaid-exempt assets and don’t count against your eligibility.

- ✓

The lookback rule matters

New York’s five-year lookback period reviews transfers or gifts made below fair market value. These can trigger penalties or delay coverage.

- ✓

Spend-down strategies help

You may legally “spend down” excess assets by paying off debts, improving your home, or converting cash into exempt resources to meet Medicaid’s limits.

- ✓

Rules differ by state

Asset limits and exemptions vary, so New York’s Medicaid guidelines may differ from those in other states. Always confirm current requirements.

- ✓

Professional review prevents mistakes

An elder law or Medicaid planning attorney can help identify countable vs. exempt assets, ensure compliance with lookback rules, and create a plan to protect your savings.

What Is Medicaid?

Medicaid is a joint program between the federal and state governments to help you pay for your medical expenses. Each state has its own plan, which the federal Department of Health & Human Services approves. New York offers funding for two types of long-term assisted care: community-based or institutional. Community-based Medicaid means the program will pay for a home health aide, housekeeping, and other services so you can stay in your home. Institutional Medicaid helps you pay for care in a nursing home.

What Do I Need to Qualify for Medicaid?

Because Medicaid is a “needs-based” program, you must pass the income and asset eligibility requirements. The state sets the income and resource limit each year. For 2021, New York automatically excludes applicants with assets above $15,900 for an individual and $23,400 for a family. For the most part, the state considers resources available to a spouse as also available to the applicant. Applicants 65 years old or older, blind, disabled, or applying for coverage of nursing home care must report all of their current assets. However, while you must report all of your assets, not everything is counted against the resource limits. These limits are based on the value of your countable assets for Medicaid, meaning resources that can be converted into cash or used to pay for care.

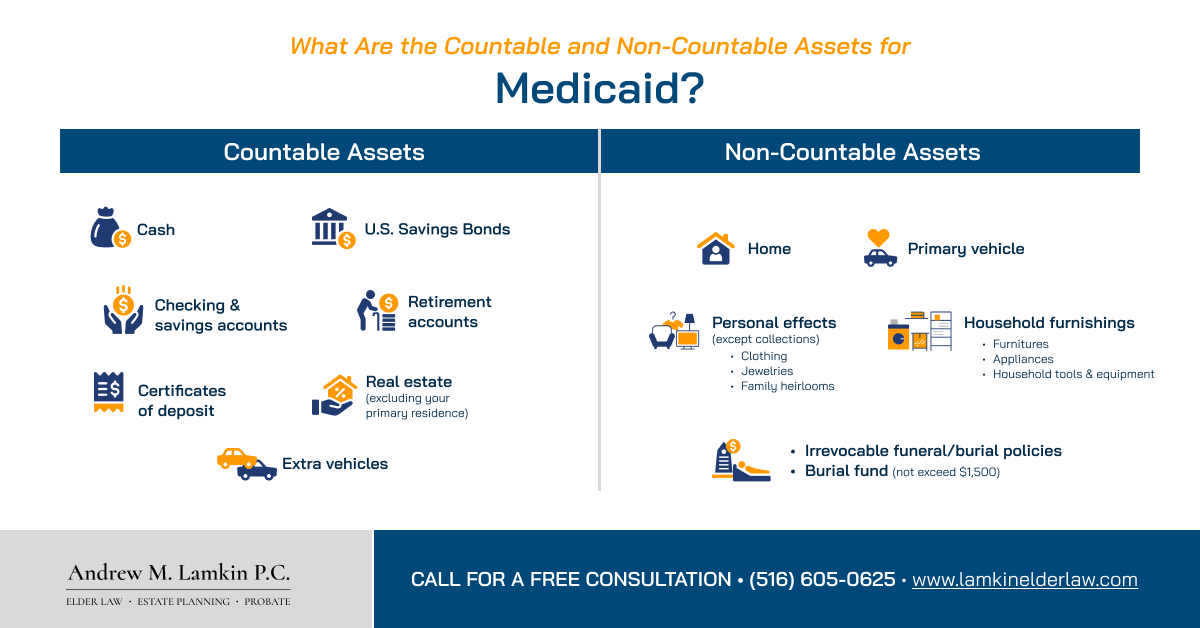

Medicaid Non-Countable Assets

Non-countable assets are things that hold value to the applicant that do not count toward the resource limit. An essential non-countable asset is your home. Your home remains a non-countable asset even if you move into a nursing home, so long as your spouse or dependent is living in the home or you have an intent to return. The idea behind this exclusion is that your home has a personal value beyond its resale value if you or your family use it as a home. Homes and primary residences are among the most important Medicaid exempt assets, allowing individuals to qualify while protecting their family property.

If you own other real property, the state will consider its value and impact on your income. The property’s equity value means the fair market value minus any encumbrances, for example, liens and mortgages. Property that produces income with a net return on equity of 6% or more is exempt up to the first $12,000. If the net return is less than 6% of the equity value, the state will count the entire equity value of the property as a resource.

The state also does not consider the value of household goods and personal effects, such as household furniture, appliances, family heirlooms, household tools, and equipment. In addition, the state does not consider your car if you or a family member are using it. If you have more than one car, the state will not count the second car if you have a medical need or use it for employment.

Finally, the state will not consider pre-need funeral arrangements so long as they are irrevocable. You can pay a funeral firm, funeral director, or undertaker in advance for your burial, and the state will not consider that agreement to be an asset. You may also set aside money in a separate account for a burial fund so long as the amount does not exceed $1,500.

Medicaid Countable Assets

Medicaid considers any resource that can be valued and converted to cash to pay for your expenses to be countable assets for Medicaid eligibility purposes. Countable assets include:

- Cash, checking, savings, credit union accounts, and certificates of deposits (CDs);

- Retirement accounts (deferred compensation, IRA, or Keogh);

- Life insurance policies with a face value over $1,500;

- A burial fund over $1,500 (or $3,000 per couple);

- Securities, stocks, bonds, and mutual funds;

- Trust accounts;

- Annuities;

- Vehicles other than your primary vehicle, including campers, snowmobiles, boats, and motorcycles; and

- Real property (other than that excluded above).

These are the most common examples of countable assets under Medicaid rules, though your individual eligibility can vary based on your financial situation and state guidelines. While this may seem like a simple list, it is not always straightforward. For example, assets in trust accounts or annuities are not always considered countable. If you exceed the resource threshold, the state will automatically disqualify you from coverage. It is a good idea to have a professional review your application, such as a legal practitioner experienced in elder law.

What are Countable Assets for Medicaid?

Countable assets for medicaid are real and personal property that can be valued and converted into cash, used to determine eligibility for programs like Medicaid.

Examples of Countable Assets for Medicaid

- Cash

- Checking and savings accounts

- Certificates of deposit

- U.S. Savings Bonds

- Retirement accounts

- Real estate (excluding your primary residence)

- Multiple cars

What Is the Lookback Rule?

New York’s lookback rule applies when the state considers your eligibility for nursing home care. The rule requires the state to “look back” for assets disposed of during the last five years. If you gave away any assets for less than fair market value, you might face a penalty period. During the penalty period, the state identifies you as ineligible for coverage for nursing home benefits.

What Is “Spending Down?”

Spending down is a plan to transfer your countable assets so that they will not count against your resource limit. Your plan can include more than medical expenses. For example, you might pay off debts, purchase a new non-countable asset, or improve a non-countable asset, such as your home or car.

How Can a New York Medicaid Lawyer Help?

An experienced Medicaid lawyer can review your assets and help you make a plan for spending down that will most benefit you, your spouse, and your dependents. At the Law Office of Andrew M. Lamkin, we understand the intricacies of Medicaid resources and know the differences between Medicaid countable and non-countable assets. Our clients have trusted us with planning for their future care for years. Contact us today so that we can help you qualify for the Medicaid benefits you deserve while protecting your assets and income for your family.

Andrew Lamkin is principal in the law firm of Andrew M. Lamkin, P.C., where he focuses his practice in the areas of elder law, estate planning and special needs planning, including Wills and Trusts, Medicaid planning, estate administration and residential real estate transactions. He is admitted to practice law in New York and New Jersey.